May 3, 2024: The latest report from the International Energy Agency presents both optimistic and confused signals over the direction of battery storage in scale for the future.

The future role of lithium batteries and potential new chemistries are the dominant themes of this 157-page report. The underlying assumptions being that the cost of energy storage with these new technologies is going to continue to fall.

For all intents and purposes, lead acid batteries have been side-lined in its analysis. A passing nod is given to the chemistry saying, “lead acid batteries generally are expected to maintain a sizeable share of the mini-grid market to 2030. The staying power of the lead-acid battery is attributable to its safety, its ability to tolerate higher temperatures and its relatively low capital cost.”

Key take-aways of the IEA report.

• Battery storage in the power sector was the fastest growing energy technology in 2023 that was commercially available, with deployment more than doubling year-on-year. Strong growth occurred for utility-scale battery projects, behind-the-meter batteries, mini-grids and solar home systems for electricity access, adding a total of 42 GW of battery storage capacity globally. EV battery deployment increased by 40% in 2023, with 14 million new electric cars, accounting for the vast majority of batteries used in the energy sector.

• Despite the continuing use of lithium-ion batteries in billions of personal devices in the world, the energy sector now accounts for over 90% of annual lithium-ion battery demand. This is up from 50% for the energy sector in 2016, when the total lithium-ion battery market was 10-times smaller.

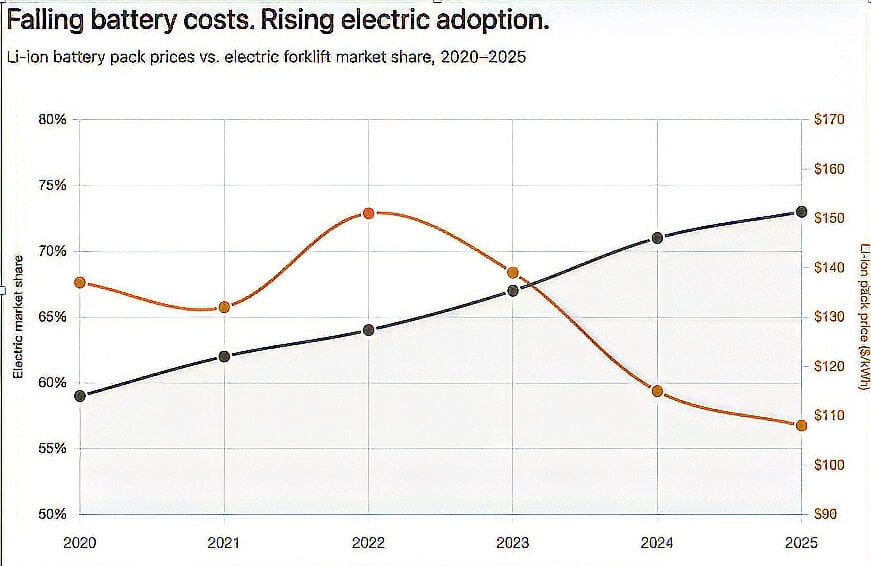

• Lithium-ion batteries have outclassed alternatives over the last decade, thanks to 90% cost reductions since 2010, higher energy densities and longer lifetimes. Lithium-ion battery prices have declined from $1,400 per kilowatt-hour in 2010 to less than $140 per kilowatt-hour in 2023, one of the fastest cost declines of any energy technology ever, as a result of progress in research and development and economies of scale in manufacturing.

• Lithium-ion chemistries represent nearly all batteries in EVs and new storage applications today. For new EV sales, over half of batteries use chemistries with relatively high nickel content that gives them higher energy densities. LFP batteries account for the remaining EV market share and are a lower-cost, less-dense lithium-ion chemistry that does not contain nickel or cobalt, with even lower flammability and a longer lifetime.

• While energy density is of utmost importance for EV batteries, it is less critical for battery storage, leading to a significant shift towards LFP batteries without any significant spill over into lead battery alternatives despite the lower price, recyclability and safety concerns.

• China is the world’s largest market for batteries and accounts for over half of all battery in use in the energy sector today. The European Union is the next largest followed by the US with smaller markets also in the UK, Korea and Japan. Battery use is also growing in emerging market and developing economies outside China, including in Africa, where close to 400 million people gain access through decentralized solutions such as solar home systems and mini-grids with batteries in order to achieve universal access by 2030.

• China undertakes well over half of global raw material processing for lithium and cobalt and has almost 85% of global battery cell production capacity. Europe, the US and Korea each hold 10% or less of the supply chain for some battery metals and cells today.